All Categories

Featured

Table of Contents

The are entire life insurance policy and global life insurance policy. expands money value at an ensured rate of interest and also with non-guaranteed dividends. expands cash worth at a repaired or variable rate, relying on the insurer and plan terms. The cash worth is not contributed to the fatality benefit. Cash money worth is an attribute you benefit from while active.

The policy financing rate of interest price is 6%. Going this path, the rate of interest he pays goes back into his policy's cash value instead of an economic institution.

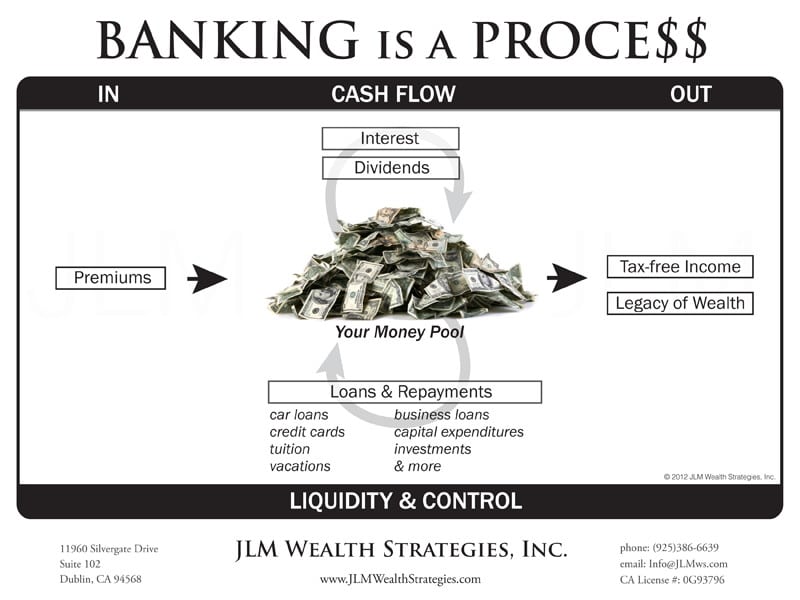

Infinite Banker

The principle of Infinite Banking was created by Nelson Nash in the 1980s. Nash was a money professional and fan of the Austrian school of business economics, which supports that the worth of items aren't clearly the result of traditional financial structures like supply and demand. Instead, individuals value money and goods in different ways based on their economic condition and demands.

One of the mistakes of standard banking, according to Nash, was high-interest prices on loans. Long as financial institutions established the rate of interest prices and financing terms, individuals really did not have control over their very own wealth.

Infinite Banking requires you to possess your financial future. For ambitious individuals, it can be the ideal monetary device ever. Here are the advantages of Infinite Financial: Perhaps the single most useful aspect of Infinite Banking is that it improves your cash flow.

Dividend-paying entire life insurance is really reduced threat and supplies you, the insurance holder, an excellent deal of control. The control that Infinite Banking offers can best be grouped right into 2 categories: tax advantages and property defenses.

Bank On Yourself Scam

When you utilize whole life insurance policy for Infinite Financial, you get in right into a personal agreement between you and your insurance firm. These protections may vary from state to state, they can consist of protection from property searches and seizures, protection from reasonings and protection from lenders.

Entire life insurance coverage plans are non-correlated assets. This is why they function so well as the financial structure of Infinite Banking. No matter of what takes place in the market (supply, genuine estate, or otherwise), your insurance coverage plan preserves its well worth.

Entire life insurance policy is that third bucket. Not just is the price of return on your whole life insurance coverage plan guaranteed, your death benefit and premiums are additionally ensured.

This framework aligns flawlessly with the concepts of the Perpetual Wide Range Approach. Infinite Banking attract those seeking greater monetary control. Here are its main advantages: Liquidity and accessibility: Policy lendings offer prompt access to funds without the restrictions of standard small business loan. Tax effectiveness: The cash money worth expands tax-deferred, and plan car loans are tax-free, making it a tax-efficient device for building wide range.

The Nelson Nash Institute

Asset protection: In numerous states, the cash worth of life insurance is secured from lenders, including an added layer of financial safety and security. While Infinite Financial has its qualities, it isn't a one-size-fits-all solution, and it comes with considerable drawbacks. Below's why it might not be the most effective technique: Infinite Banking usually requires detailed policy structuring, which can perplex insurance policy holders.

Picture never having to stress over small business loan or high rate of interest once again. What if you could borrow money on your terms and construct riches all at once? That's the power of unlimited financial life insurance policy. By leveraging the cash value of whole life insurance policy IUL policies, you can grow your wide range and obtain money without relying on typical banks.

There's no collection funding term, and you have the liberty to pick the settlement routine, which can be as leisurely as settling the car loan at the time of death. This versatility includes the maintenance of the fundings, where you can choose for interest-only settlements, keeping the loan equilibrium flat and convenient.

Holding money in an IUL taken care of account being attributed passion can often be better than holding the cash money on deposit at a bank.: You've always dreamed of opening your own pastry shop. You can obtain from your IUL policy to cover the first costs of renting a room, acquiring equipment, and hiring personnel.

Can I Be My Own Bank

Individual car loans can be acquired from conventional banks and debt unions. Right here are some crucial points to take into consideration. Bank card can offer a versatile way to borrow money for really temporary durations. Nevertheless, borrowing cash on a debt card is usually really expensive with annual percent rates of interest (APR) usually reaching 20% to 30% or even more a year.

The tax therapy of plan finances can vary significantly depending upon your country of house and the certain terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan lendings are usually tax-free, providing a substantial benefit. In other jurisdictions, there may be tax obligation effects to think about, such as prospective taxes on the finance.

Term life insurance just provides a survivor benefit, with no money worth build-up. This suggests there's no cash value to obtain against. This post is authored by Carlton Crabbe, Chief Executive Police Officer of Resources permanently, an expert in giving indexed universal life insurance policy accounts. The info provided in this article is for instructional and educational purposes just and must not be taken as monetary or investment advice.

For finance officers, the substantial regulations enforced by the CFPB can be seen as troublesome and limiting. First, finance officers frequently suggest that the CFPB's laws develop unneeded bureaucracy, leading to even more paperwork and slower financing processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) rule and the Ability-to-Repay (ATR) needs, while focused on securing consumers, can bring about delays in closing offers and increased operational prices.

{kind=link}

Latest Posts

How To Become My Own Bank

Infinite Financial

Infinite Banking With Iul: A Step-by-step Guide ...